Many credit card users set their accounts to autopay their minimum payment and go on spending. Paying $25 or 1% to 2% of your balance every month sounds easy… because it is. That’s why 45% of millennials are only making their minimum payments.

This set-it and forget-it attitude allows you to dodge late fees and keep your account in “good” standing… but that’s about it.

Unless you’re in a serious financial crisis and you need to save cash for a couple of months, only paying your minimum payment is a poor financial strategy that could end with DEVASTATING financial consequences:

You’ll Pay A LOT of Interest Over MANY Years

Credit card interest charges are determined as a percentage of your outstanding balance. The larger your balance, the greater your interest charge.

By only making minimum payments, the total interest increases each month and your balance snowballs, especially if you continue making charges to the card.

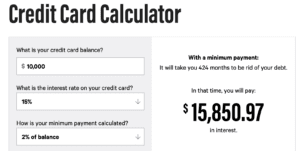

Say you owe $10,000 in credit card debt with 15% interest, and you’re making a 2% minimum payment ($200) each month.

Here’s how many years and dollars you’ll spend before your card is paid off:

That’s 35 years and $25,850.97 to pay off a $10,000 debt – and the $15,850.97 in interest is more than you owed in the first place!

Check out this online credit card calculator to calculate how much interest you’ll pay and how long it will take to pay off your debt.

If you take a look at the “Minimum Payment Warning” on your bill, you’ll find a table telling you how long it will take you to pay your balance by only making minimum payments. The longer you take to pay down your debt, the more interest you’ll rack up, and the more money you’ll end up spending.

Your Credit Score Will Suffer

The percentage of the credit you are using is known as your ‘credit utilization ratio’. This metric has a major impact on your credit score, which is why keeping a high balance is not a good idea.

The typical suggestion is to use less than 30% of your credit limit per card. But if you’re only making minimum payments, that means you’re using a larger percentage of your allowed credit, which will negatively impact your credit score.

Remember, a poor credit score will make it more difficult to qualify for loans and other credit cards. It can even impact your job prospects and your ability to rent an apartment.

Can’t Afford to Pay More Than Your Monthly Payments? Ask for Help

Paying more than your minimum credit card payment is not only beneficial but critical to your financial health. However, some of us are stuck between a rock and a hard place and simply can’t afford to pay off more of our debt.

Fortunately, there are consumer credit and debt relief solutions offered by companies like American Consumer Solutions™. According to the American Fair Credit Council, debt settlement is the most consumer-friendly debt relief option for Americans overwhelmed by debt. Contact a certified debt consultant today to receive a free debt analysis.